Posted 1/6/2023

Months of speculation have surrounded the Biden-Harris Administration Debt Relief program, but we’re one step closer to a final decision. The Supreme Court has agreed to hear oral arguments in February 2023 for two cases currently blocking the Department of Education from accepting and processing applications for the one-time student loan debt relief program.

If the program moves forward, more than 40 million federal student loan borrowers will be eligible for some relief and nearly one-third will be eligible to have their loans completely paid off.

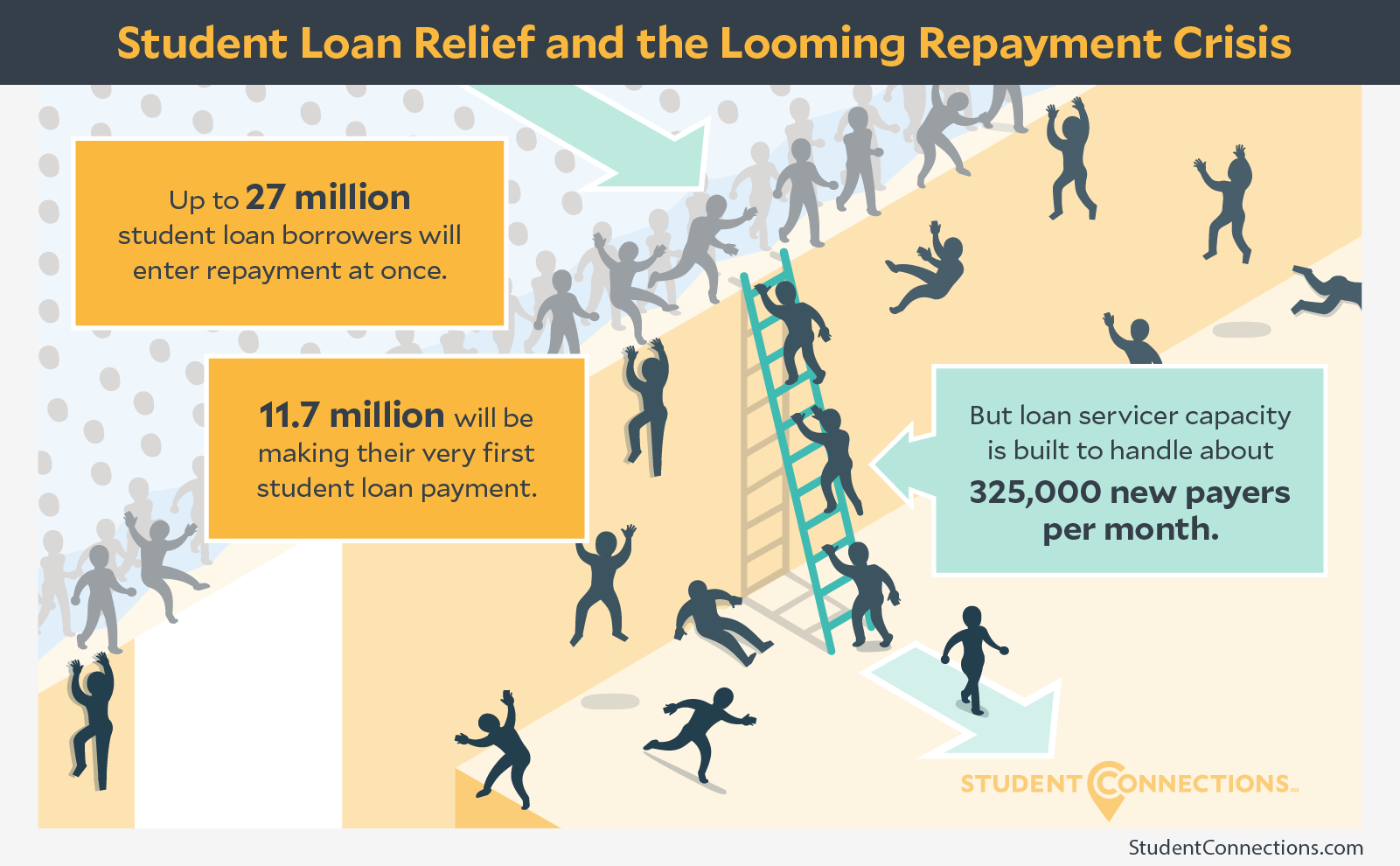

However, if the Supreme Court decides against the plan, more than 27 million borrowers1 will be expected to enter repayment just 60 days after the ruling. Borrowers who have been told they’ll receive partial or complete loan forgiveness are already expressing confusion, disappointment and anger.

In isolation, dumping 27 million borrowers into repayment at once would be a challenge. Unfortunately, this event would be compounded by several of factors.

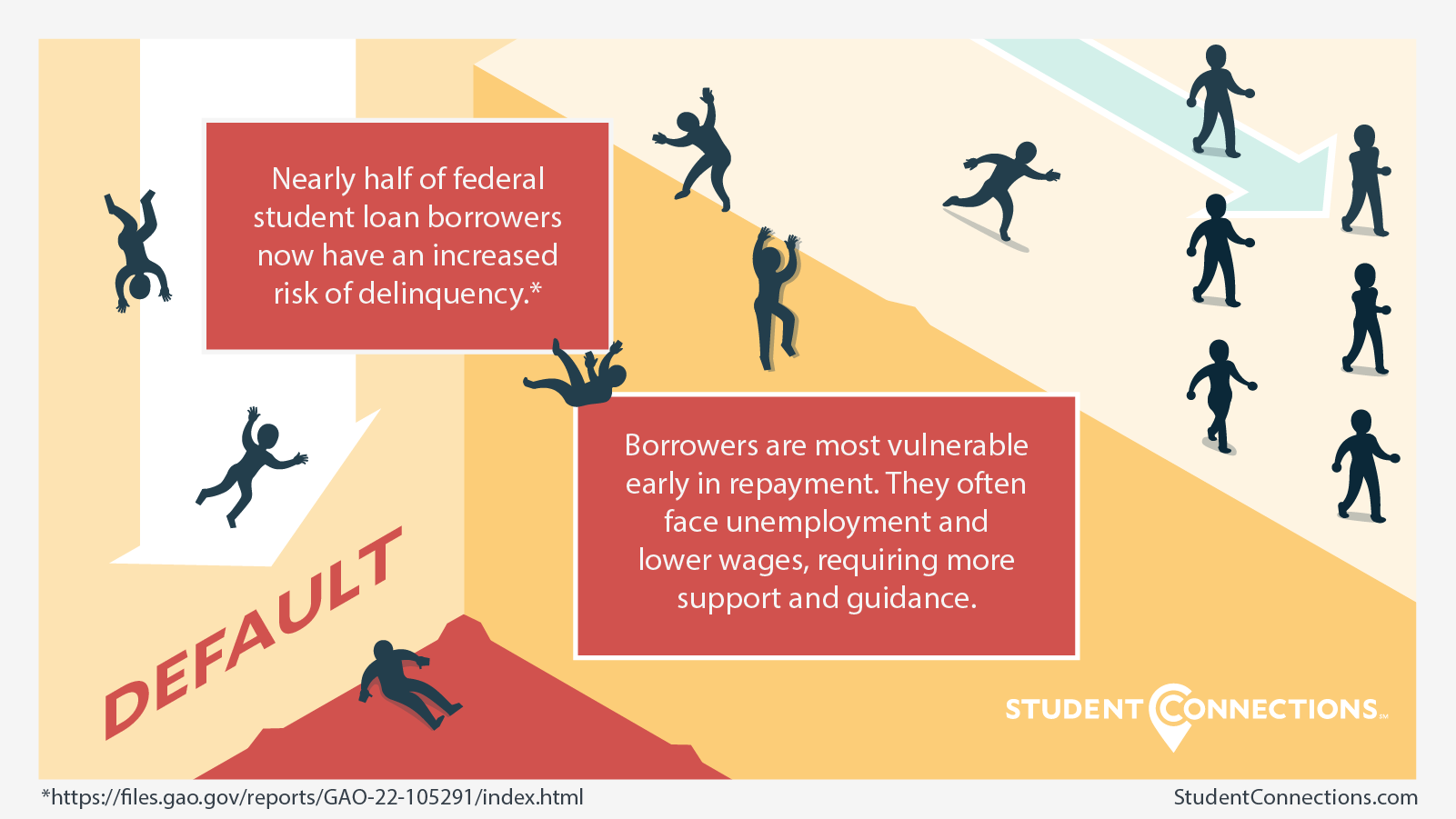

First, approximately 11.7 million2 former students will be making their very first student loan payment – ever. New borrowers require more assistance early in the process, and it’s vital they get that support. Research shows making the first few payments on student loan debt are critical indicators of long-term repayment success.

This is because borrowers in the first years of repayment are more likely to be unemployed or underemployed and require assistance from programs like income-based repayment plans. They are less likely to understand their options, necessitating additional help from their loan servicer.

Unfortunately, the systems that assist students are not equipped to handle such staggering numbers. Prior to the payment pause, the eight federal student loan servicers were set up to manage a historical average of 325,000 new borrowers entering repayment each month. Today, there are only six servicers and will be flooded by 36 times that number.

In addition, the existing loan servicers (like many companies) had to reduce their workforce during the early stages of the pandemic. They will staff-up as best they can to meet the challenge, but there’s no realistic way for them to fully prepare. This will likely result in hours long hold times, and no proactive phone outreach.

Then there’s the borrowers’ emotional state to consider. Twenty-six million3 have already applied for loan forgiveness. Many made financial choices based on what they believed was a done deal. If the relief plan is struck down, they aren’t likely to be happy, which could make communication with them much trickier.

While these unprecedented challenges will strain an already vulnerable student loan system, there are ways to mitigate the risk. Start by using your existing networks to provide the information and support your former students need to successfully repay their student loans.

Many schools simply don’t have the staff or capacity to provide borrowers with critical updates. Effective outreach requires a multi-channel communication strategy. This is where having a default prevention outreach partner can help.

Student Connections supports over 8 million borrowers on the behalf of more than 550 campuses. We use a combination of phone calls, emails, text messages, social media posts, live chat and chatbot to connect former students with the information they need to succeed.

We also take time to personally counsel borrowers who have questions or are seeking to better understand their personal options and relief when payments resume. Our experienced team of borrower advocates have provided counseling to more than 700,000 borrowers throughout the entire payment pause.

Contact us to learn how we can help your borrowers.

1Assumes that repayment will begin in June. Based on average number of borrowers typically entering repayment each month, multiplied by 39 months since the payment pause began in March 2020.

2Includes 26 million in forbearance and repayment, plus 1.3 million in grace as of 12/31/22. Source: Federal Student Aid

3Reported Nov. 3, 2022. Source: The White House Briefing Room