Posted 2/15/2023

It’s been a wild three years. Pandemic, economic turmoil, and unprecedented federal actions rocked the normally sedate world of student loan repayment. Today’s borrower looks substantially different from their December 2019 counterpart. As we enter 2023, it’s important to examine the key factors shaping borrower behavior and prepare for the challenges they represent.

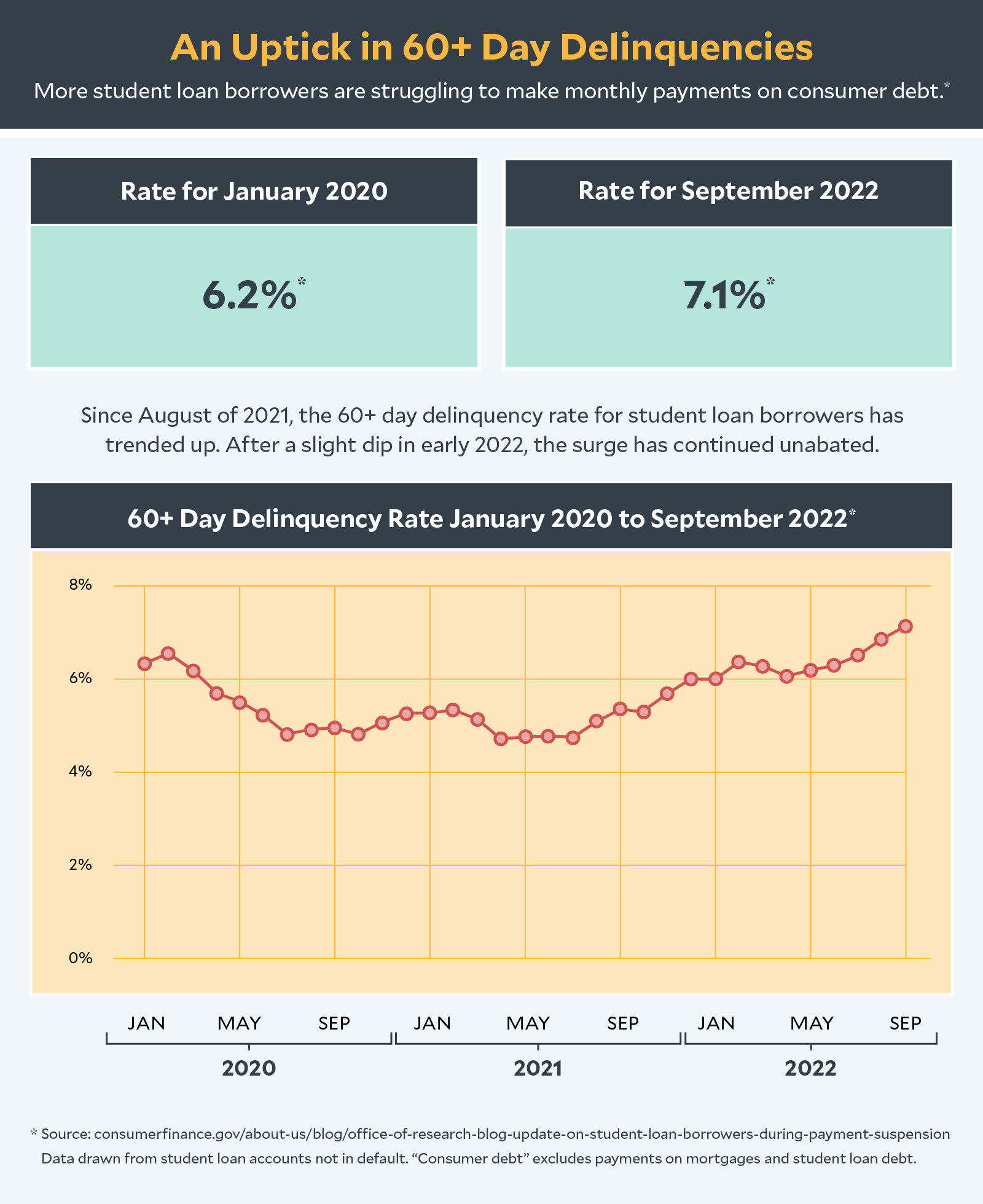

A recent article by the Consumer Financial Protection Bureau (CFPB) warns that credit delinquency has increased among student loan borrowers. The report (which excluded mortgage and student loan debt) found the 60-day delinquency rate on consumer credit stands at 7.1%. That’s almost a full percentage point above the pre-pandemic rate of 6.2%. Delinquencies dropped well below 6% for much of 2020 and 2021 before beginning a fairly consistent climb in late 2021.

This trend shows more student loan borrowers are struggling to repay creditors at a time when they aren’t required to make student loan payments.

Supporting the CFPB’s finding is a survey from May 2021, which asked respondents the likelihood they would miss a monthly debt payment within the next three months. On average, those with student loan debt estimated a 13.5% chance they would miss a bill. Those without student loans guessed there was only an 8.7% of missing a bill.

At the time the survey was conducted, the payment pause was active but due to end in September 2021. Even without the burden of a monthly student loan payment, and the resumption of payments four months away, student loan holders still estimated a 4.8% higher chance of them missing a payment.

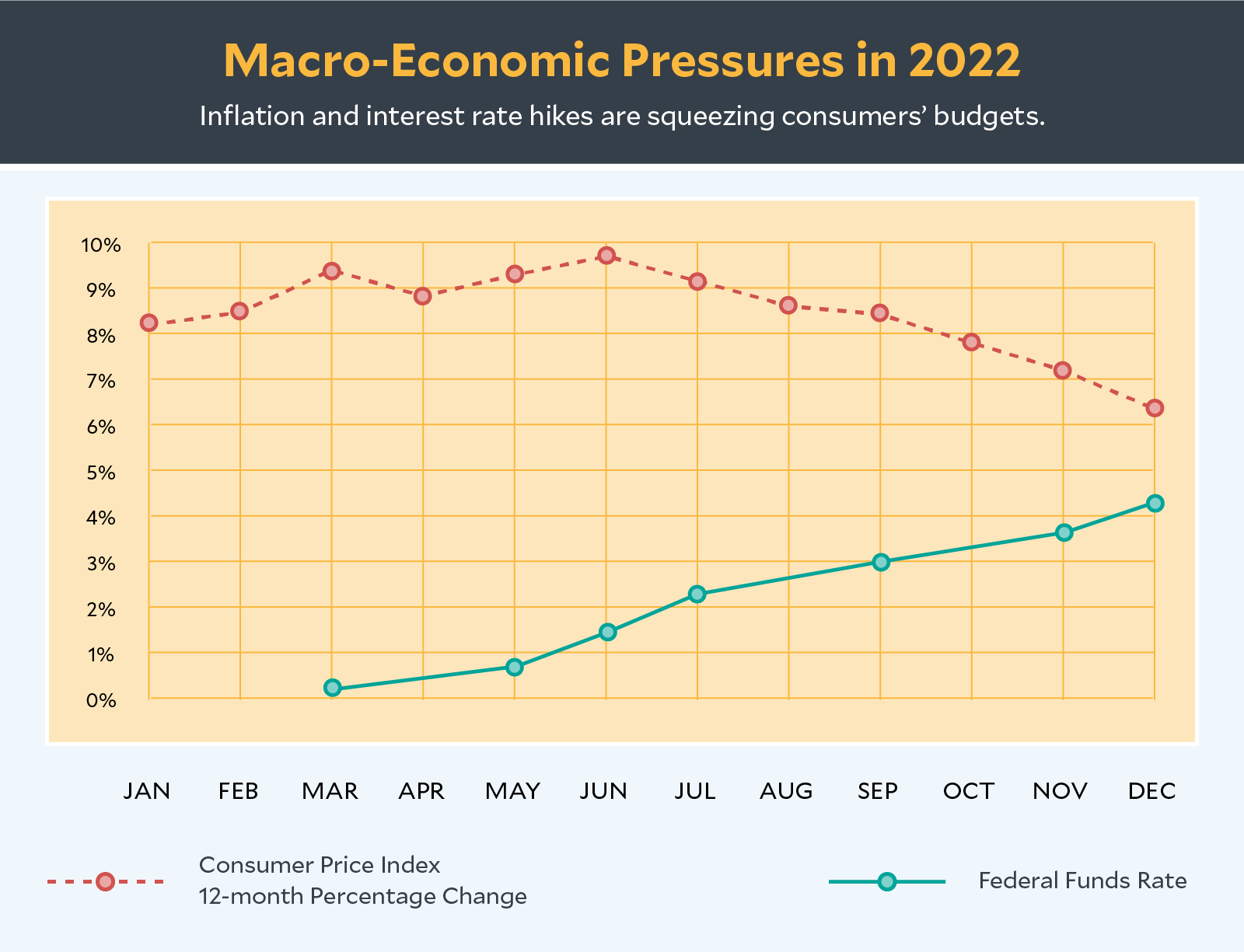

In June 2022, the 12-month US Consumer Price Index (CPI) percentage change stood at 9.8%. This represented inflation on a scale most borrowers have never experienced. The impact on individuals varied by factors such as income and location, but we can assume the increased cost of goods has strained many borrowers’ budgets.

In response to rising inflation, the Federal Reserve increased interest rates five times over the last eight months. These rate hikes were meant to curb spending and reduce demand on goods and services across the economy. The measures seem to be working as the 12-month CPI percentage change dropped to 6.5% in December 2022.

However, raising interest rates creates a risk for workers. Employers may cut jobs in the face of slowing revenue. At present, the impact of rate hikes on employment has been limited. However, Fed Chairman Jerome Powell made it clear inflation is not under control and more interest rate hikes are on the way.

Rising interest rates also impact the cost of consumer credit. Those seeking car loans will encounter higher rates on one of the more expensive sources of non-mortgage debt. Monthly payments on variable rate credit sources (like credit cards) will also rise as lenders adjust to the Fed’s moves. Keep in mind that borrowers are paying credit for goods purchased at already inflated prices.

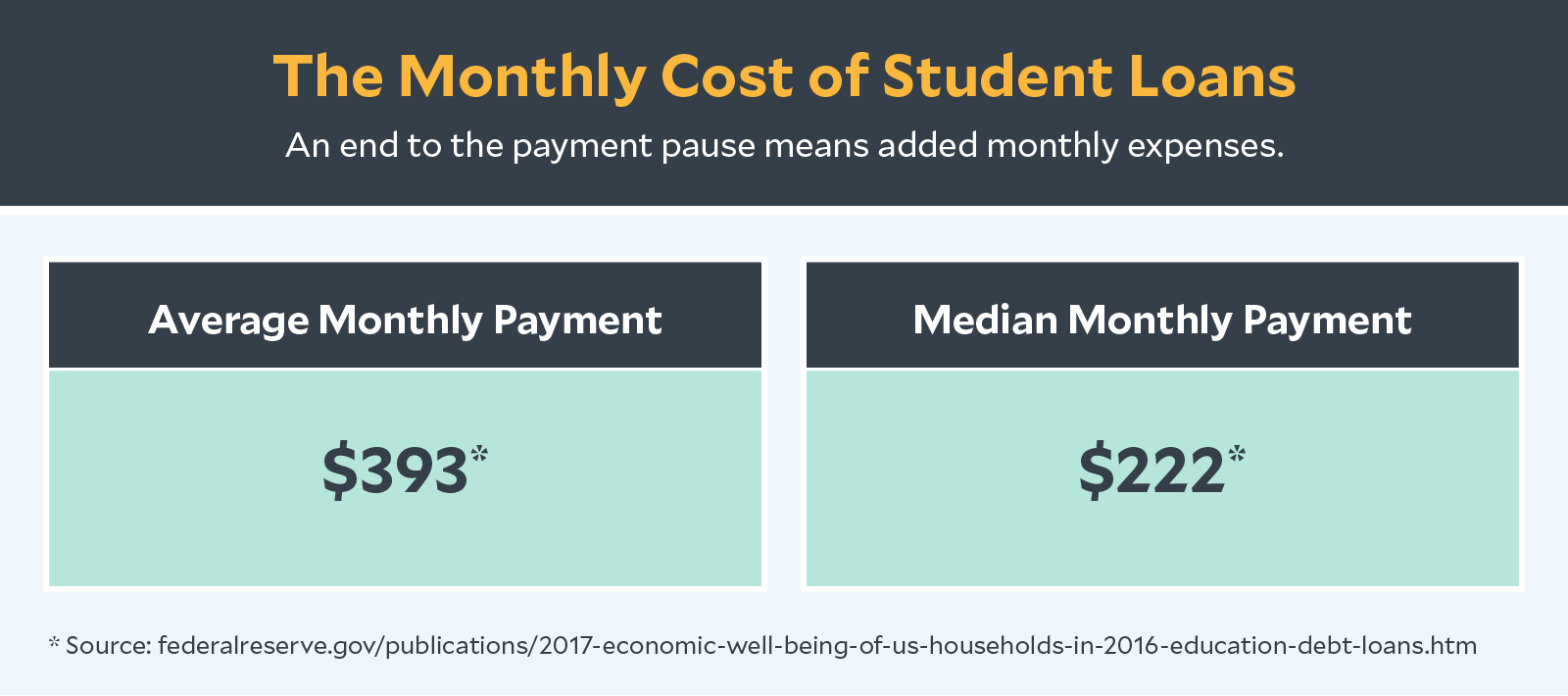

This puts additional pressure on already strained household budgets. In fact, 46% of student loan borrowers have experienced a 10% increase in their monthly consumer debt payments since the start of the pandemic. This figure excludes both mortgage and student loan debt.

In February 2023, the US Supreme Court will hear two cases against the Biden-Harris Administration Student Loan Debt Relief program. A decision is expected no earlier than late spring of this year.

If upheld, the program will erase $10,000 to $20,000 from the loans of about 40 million borrowers. Almost one-third of borrowers owe less than $10,000. Eliminating monthly student loan payments will make it easier for them to contend with rising inflation and interest rates. Borrowers with a balance remaining after relief is applied should have lower monthly payments.

The effect of the Court ruling against debt relief is difficult to quantify. Borrowers who were promised relief will see another monthly, multi-hundred dollar bill added to their already strained budgets. At the very least, we can expect them to be angry.

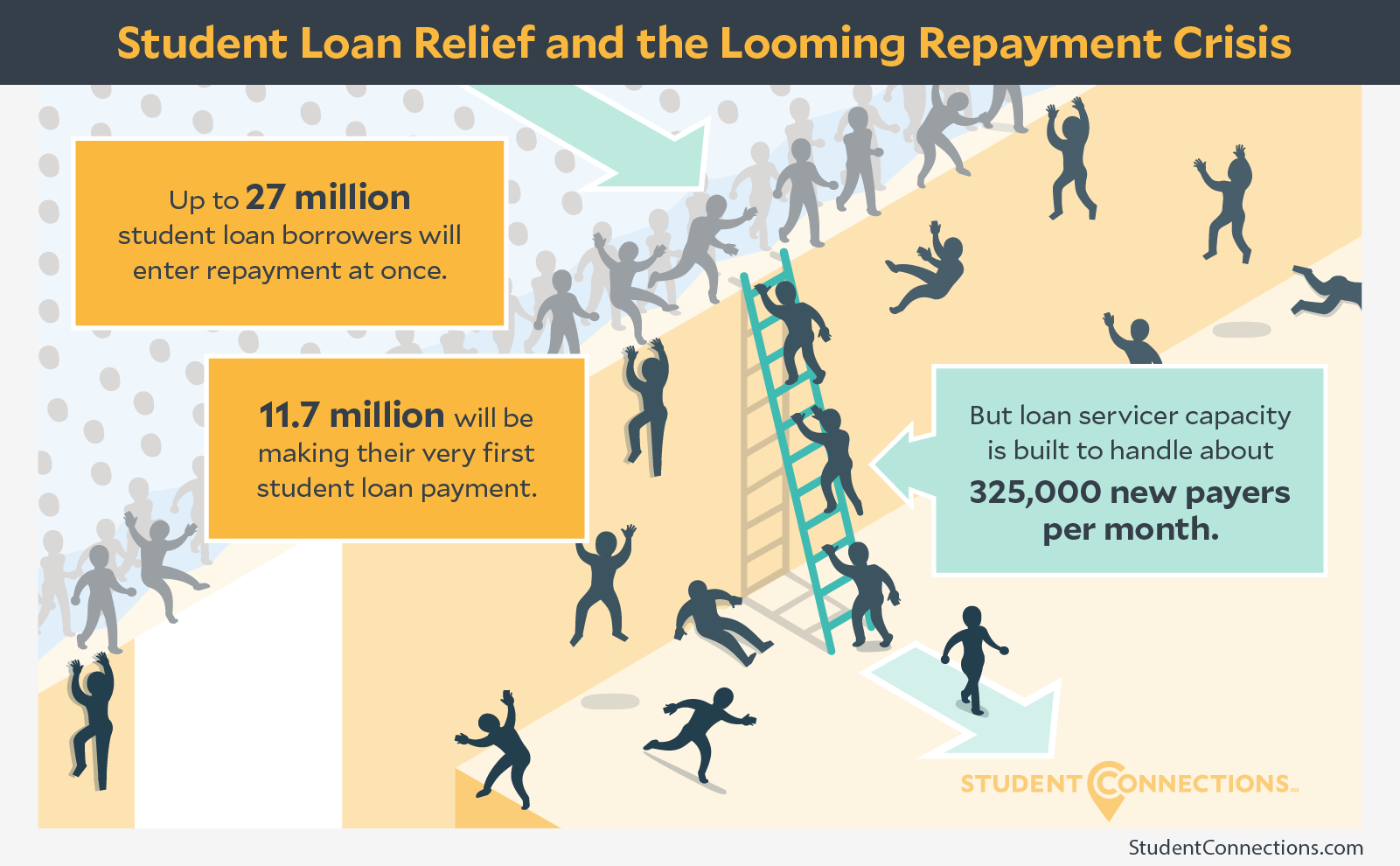

Borrowers will face more headaches when monthly payments restart in mid-to-late 2023. Up to 27 million borrowers will enter repayment at once. Depending on the Court’s decision, as many as 11.7 million of them will be completely new to repayment.

They’ll run into a system that was never expected to process more than a few hundred thousand students each month. Borrowers who are financially vulnerable may find it impossible to get help before they slip into delinquency. We dig deep into the impending repayment crisis in this post.

The resumption of monthly student loan payments will be accompanied by a surge in delinquencies. Our prediction is based on the facts laid out above. We believe they support two main conclusions:

After monthly student loan payments resume, borrowers will have another large monthly bill. Those with strained budgets may reach out for assistance. Unfortunately, they’ll find the system overwhelmed. Unable to get help and forced to choose which bills they will pay this month; many borrowers will opt to skip their student loan payment.

There are steps you can take now to minimize the impact of the repayment crisis on your former students and organization.

Start by using your existing networks to:

Many schools don’t have the resource to provide borrowers with critical updates. This is where Student Connections can help. We use a blend of phone calls, emails, text messages, social media posts, live chat and chatbot to connect former students with the information they need to succeed. Our experienced team of Borrower Advocates provides personal counseling to borrowers in need of guidance and assistance — assisting more than 700,000 borrowers throughout the payment pause.